Ahmad M. Butt of Jetstone Asset Management has written an insightful series of articles titled “Unpacking Alpha in Venture Capital”.

The highlights and key take-aways of the 4 chapters include:

Chapter 1: Setting the Context

- Dollars should be focused into capacity constrained strategies that are attacking the early stages. VC does not scale.

- Most early stage investors waste the informational alpha generated by VC — it provides a lens into what will work in the future but in nearly every scenario tells you what is not working within the incumbents. Cross-pollinate this information to unlock more alpha in you public portfolios.

Chapter 2: A Brief History of VC & Some LP Myths

- Company returns to funds are Power Law distributed which is counterintuitive to conventional risk adjusted investing. Simply put, 80% of the returns come from 20% of the deals.

- Two major themes over the last decade in the asset class: (1) the proliferation of broader participation at the earliest stages (angels, accelerators, crowdfunding etc.) and rise of the “lean startup” in a mobile driven era; and (2) the influx of non-traditional capital at the later stages (Public market investors, Corporates, Sovereign Wealth Funds and the most high profile being the Softbank Visions Fund) and the rise of the “unicorn”.

- There has been a structural shift in the capital allocations between private and public markets in favour of private companies

- Venture doesn’t scale and value creation is derived from capturing businesses at the early stages pre-inflection point and the hyper growth phase.

- More reputable VCs, in general, exhibit less local bias and are comfortable with investing internationally and in fact out-performance has been driving by non-local investments.

Chapter 3: Unpacking Alpha Generation in VC

- The issue with Alpha generation in venture capital is that it is both extremely poorly articulated and attributed (compared to the public markets) nor supported by data.

- Access to Deals: The decline in persistence of performance over the last decades and the performance of new managers shows that it is hard to argue that firms have some structural barrier to entry and have freedom to select the best deals.

- The best entrepreneurs (who drive the outlier returns) would most likely have found the ways to create value without the hand-holding of their VCs

- By virtue of deductive reasoning in the fact that good counter-arguments exist for access and value add driving superior and consistent outperformance in venture capital, the author reaches the conclusion that unless it is all luck, venture capital, as an investment profession, must be truly about the formulation and execution of investment strategy, process and portfolio construction and management

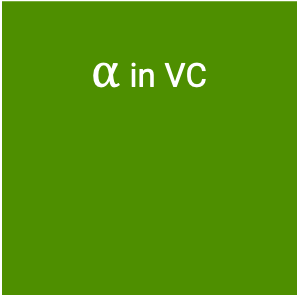

- Smaller funds have greater long-term persistence than larger funds

- There is no strong evidence that VC returns are enhanced by specialisation

- Ultimately, generalist firms that can rapidly appraise and capture the inherent value in technological breakthroughs have historically captured the outlier returns.

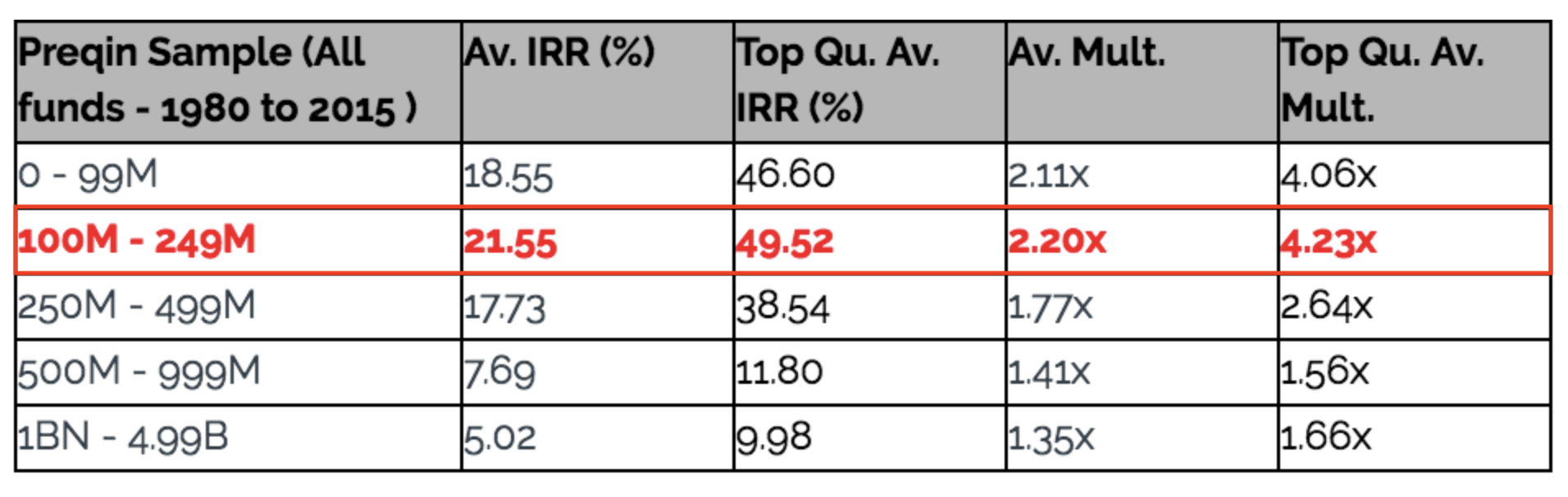

- VC as an investment class demonstrates clear auto-correlation via the now-established virtuous circle of strong subsequent fundraising driven by LP risk assessment weighting persistence of performance but the link to subsequent exits is not clear.

- VC ultimately shows mean reversion. Initial success matters for the long-run success of VC firms, but that these differences attenuate over time and converge to a long-run average across all VCs.

Chapter 4: Solving for the Human Capital Challenge in Venture Capital

- The churn in top tier performance is drastically increasing as the VC market matures and alpha is dispersed due to the inherent inefficiencies. Only the best funds plan for succession.

- As with any investment field, unconventionality is required for superior investment results. This means VC managers must be able to identify an “edge” and in this asset class the available edges are found truly looking at “frontier” technologies that other investors are not willing to evaluate; looking at industries where previously technology has had limited application; or investing in geographies that have a scarcity of competition.

- If we have isolated that individual manager hustle, investment analysis and strategic skill is the driver of returns supported by an auto-correlation of brand, network and fundraising then we need to solve for all these elements in individuals.

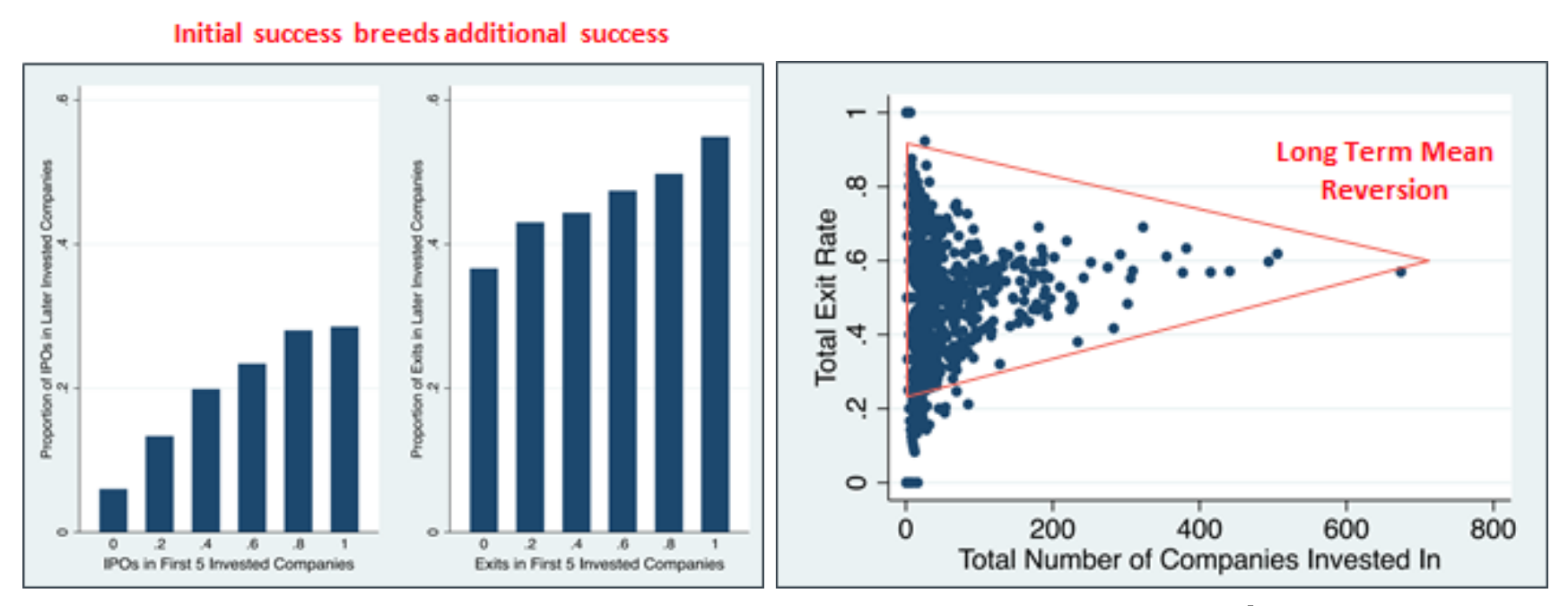

- The following table summarises the authors attempt to test and attribute key factors for alpha creation in venture capital.